Lifestyle Transition Planning - 7 Steps to Success

It’s time to move, make a change and transition to that home and property of your desire. Making moves like this are often necessary due to employment, life change, and finances. Making the transition from one place to another might also be more complicated than just selling and moving. In order to make a smooth transition one must consider the financial, emotional impact and also the logistics. We have provided this Guide with an accompanying Transition Impact & Roadmap Planner to help you think about and plan your next big move.

Step 1: Why are you considering a move?

Are you considering a move because you are being transferred, taking a new job, wanting to downsize or just ready for a change of lifestyle? Regardless of the reason, moving is a very big decision and often easier said than done. Moving also can be very expensive, stressful and disruptive. Think about the impact moving will have on you, your family and your budget. Here are some of the things you should consider.

- Packing, Moving and Storage Costs

- Real Estate, Lending and Utilities Activation Fees

- Temporary Housing Requirements

- Impacts of Disruption of School, Work and other interests

- Travel and Relocation Related Costs

If the benefits outweigh the potential costs and disruptions, making a firm decisive move decision is the first and most important step in the process.

Step 2: Where will you be moving and why?

Depending upon what is driving your move decision, the general location and specific type and characteristics of your future lifestyle property is key. Knowing where you are going and what to search for will make a huge difference in the time you spend searching for, touring and ultimately selecting the right property. Distance is also a big factor. With the internet and the latest digital marketing tools available to allow you to search online, see the property and even tour it through available 3D tour software, you have enough at your disposal to see much of what you need to see to get a feel for what properties are available, costs, estimated taxes etc. Most cities and towns have websites with community information, details on schools, things to do, local shopping and dining. To gain a full profile on and analyze the area you should prepare a list of the selection criteria that are most important to you. Here are some examples:

- Proximity to Employment

- School Rating State/National

- Crime Rate

- Population

- Local Property Tax Rate

- Income and Sales Tax Rate

- Local Job Market

- Local Attractions

- Dining and Shopping Options

- Churches

- Community Organizations

Once you check the boxes on the above details, it is very important to visit the area, explore the attractions, connect with the community and get a good feel for what life will feel like in your new community. One way to experience the community is to find a place to stay. Ideally, an AirBNB rental would be a nice way to experience the neighborhood. That way you can gain a better sense of home living, neighborhoods, commutes, schools, shopping, dining, etc. Make sure to check out local grocery stores, restaurants, schools, parks and attractions. Perhaps attend a local church, to meet the people and ask questions about the community.

Knowing where you will be moving will help to narrow the new property search and inform you such that you can make a confident choice of the area that best suits you.

Step 3: What are the desired characteristics of your new lifestyle property?

Knowing what you like, want and need will help you narrow the search for just the right property. It is important to take into consideration your living and space requirements, floor plan preferences, lot size, and neighborhood amenities. For example;

- Do you prefer urban or suburban living?

- Single family detached, townhouse, or condo?

- Do you want a large yard, zero lot line or acreage?

- What neighborhood amenities are important, like pools, walking trails, homeowners association, lakeside or unrestricted country property?

- How many living square feet?

- How many bedrooms? Size of bedrooms?

- How many Bathrooms? Mud shower, Tub?

- Do you prefer single level or multi-story?

- Media Room?

- Office?

- 3 Car Garage?

- Granite, Quartz or Stone Countertops?

- Wood, Ceramic or Carpet Flooring

It is important to document your preferences, including favorite interior and exterior colors, architectural style and appliance type and color. If possible, identify your absolute requirements and desired features. Don’t forget to also consider your budget, what you can afford now and perhaps add later. Being organized focused on what you require versus want, will save you time, help you make a good purchase decision and maximize your equity position in the home.

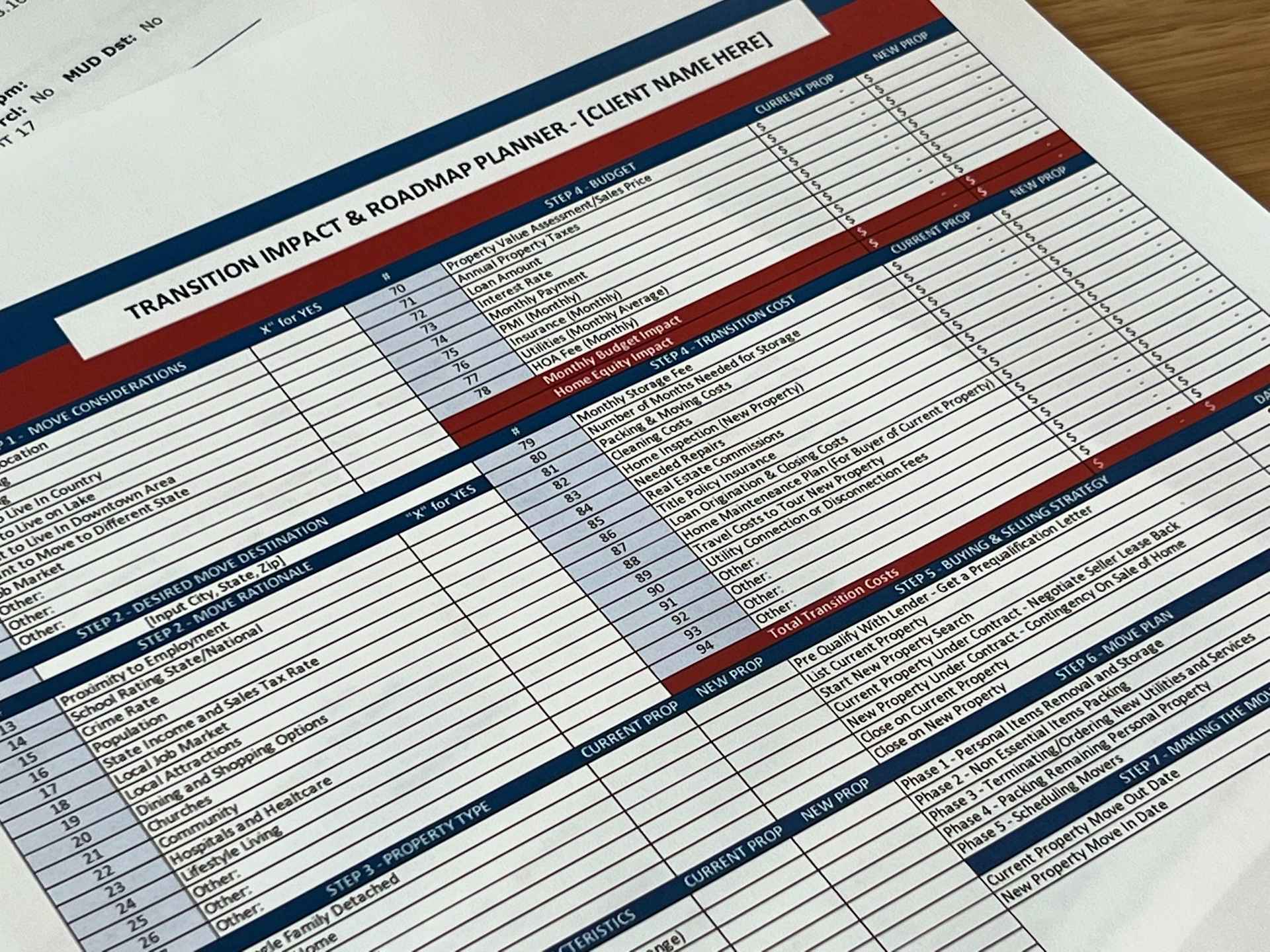

Step 4: How much money will you budget?

Once you have a feel for where you would like to live and what your requirements are it is very important to consider the costs associated with purchasing the new property as well as the budgetary impact the purchase will have. Buying too much house for your budget can put additional strain on an already stressful transition. Getting a clear picture of your budget and expenses will help you to move forward with confidence.

One way to ensure that you are being cautious is to align your new property budget as close as you can with your existing budget. If you are downsizing, and want to save money, work up a new budget that reflects your goal and plan accordingly. If you will be needing third-party financing, make sure to find a lender that has the right products and loan types to help you. Meet initially with the lender to complete a preliminary loan application that will enable the lender to help you prequalify for a loan. The lender will ask you to provide financial and credit details so that they can identify your debt to earnings ratio and determine a maximum loan amount. The lender should also be able to tell you the prevailing interest rate, loan terms and costs so that you will know your limits. The lender will also prepare a Pre qualification Letter that will provide sellers of properties you are interested in with an assurance that you have been reviewed and have basic credit worthiness to be considered as a serious buyer should you decide to make an offer.

Dealing with the cost of the home is only part of it. There are property taxes, homeowners associations fees, and mortgage and homeowners insurance that will need to be considered. Home Inspection, Moving, Relocation, utility start up, and other costs are also common. It’s critical that your budget includes those items so that you will have the whole picture.

Getting the numbers, knowing the numbers and having a clear understanding of the numbers will help you move forward with confidence, be in a better position to negotiate and ultimately make a sound and non-emotional buying decision.

Step 5: What is your Buying and Selling Strategy?

You have made a decision to buy a new home, and you have been looking for a property that meets your needs, criteria and budget. You currently own your home and the question is, how can you buy a new home while still owning your current home. Being able to coordinate the sale of your existing home while timing the search and eventual purchase of your new home is a challenge. To do this effectively you will need a solid strategy. Generally speaking buyers or sellers markets do not usually favor you on both the selling and buying side of the transaction. Therefore, careful planning and a solid strategy will make or break you.

As a buyer you will fit one of these three scenarios. Scenario 1 - You have cash resources to buy a home while selling your existing home. Scenario 2 - You need to sell your current home in order to qualify to purchase the new one. Scenario 3 - You have sufficient credit and cash flow to do a bridge loan affording you the opportunity to buy the new home, paying interest only on the new home note until you sell your existing home. Only Scenario 1 is straight forward.

Most people are in Scenario 2 by circumstance or by choice as bridge loans are expensive and not for everyone. So we will focus primarily on a strategy for Scenario 2. How would that strategy work?

The first step in Scenario 2 strategy after you have made all the above decisions is to put your current home on the market. Getting your home under contract will give you maximum leverage in the buying process. Along with getting you home on the market, you should be actively searching for your new home. The ideal scenario is that you time the sale of your home with the purchase of your new home. You close on the sale of your existing home and the next day you close on your new one. Rarely does it work like this.

Most likely you will need to make arrangements for temporary living, either a month to month rental, AirBNB or a relative who is willing to let you stay with them for a couple of months if necessary. This can be a very uncomfortable and costly short term option as it will necessitate a two stage move with a place to store your furnishings and personal property. The other option is that you negotiate a Sellers Lease Back for the time you will need to contract and close on the new property. Usually it takes 30-45 days from the execution of a sales contract to closing, if you negotiate with the sale of your existing property a 30 or 60 day Seller’s Leaseback you should have enough time (provided you have found a suitable new home) to close on your existing property and satisfy any of the lending and title work timeline required to close on your new home.

You will also need to buy your new home with a contingency for the sale of your existing property. Otherwise, you will be obligated beyond what you can qualify for. Many Sellers will not consider a contingency for sale of an existing home unless the home is under contract. So it's super important to get your current home listed as soon as possible. Doing a contingency with Seller Leaseback can go a long way to bridge the gap between closings. This is where your realtor can be a real asset with helping to develop, negotiate and execute the strategy.

There are also some very creative bridge loan options available to help make this process smooth, eliminate the contingency and make your buy side negotiation more compelling for the seller. Your Realtor should have some lender contacts that offer these types of programs.

Step 6: The big move. How will you make it happen?

Moving is always a challenge and a very disruptive experience. Here are some options to consider to make your move less stressful and effective.

Phase 1 - Personal Items Removal and Storage.

Before you put your home on the market, take the opportunity to discard any items that you no longer use or need. To prepare and stage your home for showing, remove and pack personal items like family photos, momentos, and other items that could be distracting for the buyer when they come to see your home. Your objective is to make the space more open, neutral and desirable.

If possible rent a storage unit for a short period of time so that unnecessary items in both the home and garage can be stored temporarily while you are showing the home. It is very important to declutter and open up the home to be seen and to have the appearance of ample storage space.

Phase 2 - Non Essential Items Packing.

When the home is under contract you should start the second phase where you will start to pack all non essential living items including extra seasonal clothing, stored cleaning supplies, dishes, extra bedding, towels and decor. Be sure to label all boxes and bins with the names of its contents, and the room it came out of. It is a good idea not to start moving furniture until you close on the sale because it is more difficult to show and sell an empty home.

Phase 3 - Terminating and Ordering New Utilities and Services

Prior to closing on your existing home you should notify all of the utility companies that you plan to move and terminate services. They will ask you the date of termination. You should coordinate this with the next phase of moving so that your termination date is the same day or one day after your move date. For some utilities, transferring service to the new buyer will save them money, so work with your realtor to coordinate transfers with the new buyer.

If you are remaining in the home on a Seller Lease Back, you will want to keep the utilities and services active in your name until you move.

Weeks prior to closing on your new home you should contact the utilities and services providers servicing the new home and order service. You should try to transfer services from the seller to you when possible to avoid interruption and expensive disconnect and reconnect fees. You should be able to coordinate this through your realtor.

Phase 4 - Packing Remaining Personal Property.

After closing your existing home, and new home is the time to start packing the remaining items in the home. Remember to label all boxes and bins with the names of its contents, and the room it came out of. If you are requiring a Seller Lease Back, and have not closed on your new home, you should time your move with the closing date of your new home

Phase 5 - Scheduling Movers.

With most of your items packed. Movers should be scheduled well in advance. You should contact and interview several moving companies to get a sense of their services, pricing and schedule availability. Moving companies are NOT all the same. Make sure to check out reviews, check references and ask people you know who have moved recently about their experience and who they worked with. The mover makes a very big difference in the safety of your belongings and the stress of moving.

Step 7: Making the move and adapting to your new lifestyle.

With your current home now sold and your new home ready, it’s time to move. The best time to thoroughly clean a home, windows, light fixtures, appliances, carpets, air ducts and fireplaces is while the home is vacant. MAKING MOVE A BREEZE Other small projects like patching, painting and installing carpet, flooring, shelves, fans and fixtures is also easier when the home is empty. If possible, plan time in your move schedule to complete these tasks.

Prior to loading up the non-boxed furnishings in your current home, you should consider taking a photograph of the item before it is loaded. These photos can document the condition of items prior to loading and transport. Having these photos later will help you provide evidence should any of the items become damaged during the move. Most movers should cover damage claims. Also, as boxes, bins and furnishings are loaded, each should be carefully inventoried. Most reputable movers do this as a best practice.

The day of the move into your new home you should consider placing a Blue Painters Tape Label on the door of each room in the new house. Instruct the movers to move the clearly labeled bins and boxes into the respective rooms in order to make unpacking easier. Make sure to inspect non-boxed furnishings for damage. If you find any damaged items immediately take a photo of the damage and log the damaged item as a claim with the mover. Your previous photo of the undamaged item will be critical evidence of your claim. Also, check off items that were previously inventoried so you will be able to account for any lost items.

With the move completed take your time unboxing and don’t overdo. Try and relax, take in the new neighborhood, go meet the new neighbors and enjoy your new surroundings. Give yourself a huge pat on the back for making a Transition Plan, and executing that plan.

A Good Realtor Can Make a Huge Difference

At Equitus we do not limit our role to just helping you buy and sell a property. Yes that is a huge role, but we also believe we can and should be your advocate every step of the way. If there is anything we can do to help facilitate the successful outcome of your transition, we are committed to do that. With each of these steps, we can advise, coordinate, facilitate and help you with contacts, services and recommendations. You do not have to go it alone. Let us help you first by sharing this document and the accompanying transitions plan kit to help you organize your thoughts and develop a workable plan. Next, let's get together and find areas in the plan where you would like us to help. Together we can make this process a success.